It was a Tuesday afternoon in early March when I first encountered Gladys Santiago — not in a hospital waiting room or a legal aid office, but at a BP gas station off Wake Forest Road in Raleigh, North Carolina. She was standing behind me in line, phone pressed hard against her ear, her voice low but strained. I caught fragments: denied again, appeal deadline, I don’t have that kind of money. When she hung up, I introduced myself. By the time we’d both paid for our gas, she’d agreed to talk.

We met two days later at a diner near her apartment in northeast Raleigh. Gladys Santiago, 52, has worked as a pharmacy technician for nearly eighteen years — most recently at a regional pharmacy chain where she processes insurance claims and manages medication inventory. She is precise, methodical, and quick with numbers. She is also, as she told me within the first ten minutes, in a financial situation she never expected to be in at this stage of her life.

A Raise That Changed Everything — and Then Didn’t

In August 2024, Gladys received the best news of her working life: a promotion to lead pharmacy technician, bumping her annual salary from $42,500 to $51,200. After years of incremental raises, she finally felt financially stable. She told me she cried in the parking lot after her manager called her into the office.

What followed, she now describes with visible regret, was a cascade of reasonable-seeming decisions. She moved from a shared two-bedroom apartment — where she paid $780 a month toward rent — into a nicer unit where her share was $1,050. She financed a used 2022 Honda Civic, adding a $387 monthly car payment. She upgraded her phone plan, started a meal kit subscription, and put a gym membership on autopay. None of it felt reckless at the time.

By October 2025, Gladys had roughly $1,100 in her savings account — down from $3,400 the previous year. Her take-home pay had increased by about $540 a month after taxes, but her fixed monthly expenses had grown by nearly $700. She was, for the first time in years, quietly running a monthly deficit and drawing it down from savings without fully acknowledging what was happening.

The Fall That Set Everything in Motion

On November 14, 2025, Gladys was restocking shelves in the pharmacy’s back stockroom when she slipped on a wet floor near a utility sink. There was no wet floor sign. She fell hard onto her right side, fracturing two ribs and badly spraining her right wrist — her dominant hand. She was taken by ambulance to WakeMed Hospital, where she spent most of that Friday in the emergency department.

Gladys filed a workers’ compensation claim with her employer the following Monday. She had documentation from WakeMed, a written statement from a coworker who witnessed the fall, and photos she had taken of the area before leaving that day. She assumed the process would be straightforward. According to the North Carolina Industrial Commission, injured workers in the state have up to two years to file a workers’ comp claim — but the early filing is critical to preserving rights during a denial.

The insurer’s denial letter arrived on January 9, 2026 — fifty-six days after the incident. The stated reason: Gladys had allegedly failed to follow proper workplace safety protocols by entering the stockroom without checking that the area had been cleared for use. Her employer’s account of events, she told me, did not match hers or her coworker’s.

What the Denial Actually Cost Her

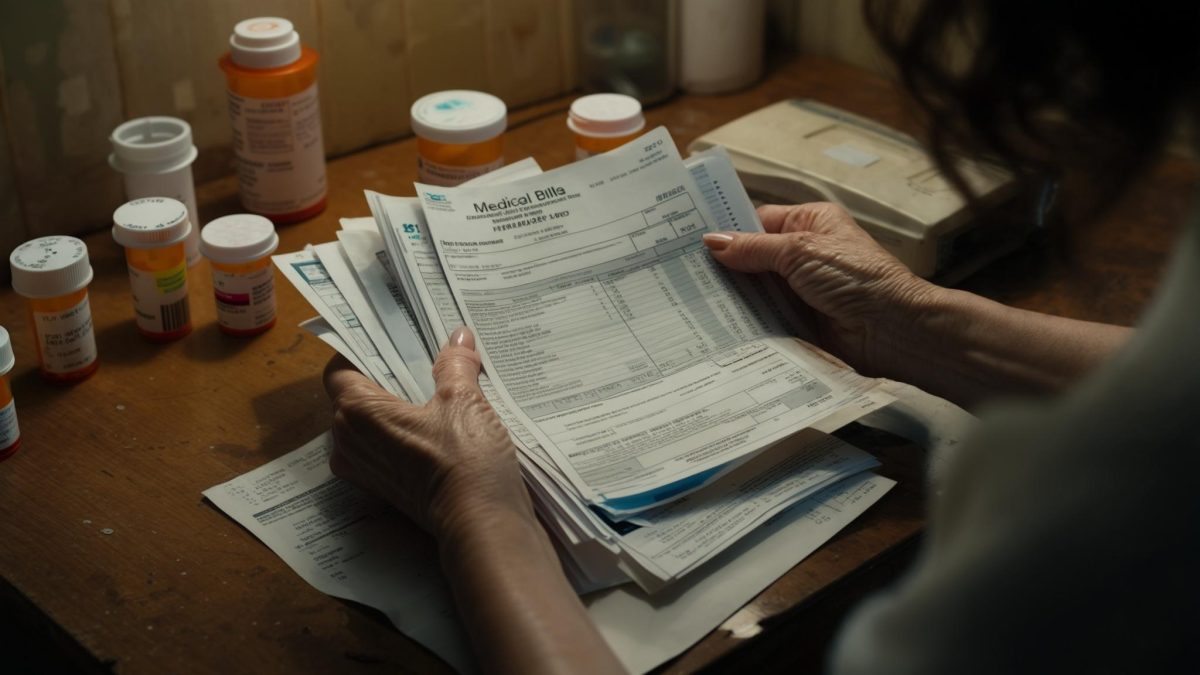

When the claim was denied, every bill from her injury shifted from the workers’ compensation system — which would have covered 100% of medical costs and paid two-thirds of her wages during recovery — onto her personal health insurance and her own bank account.

Gladys’s employer-sponsored health plan carried a $4,500 annual deductible. She had not yet spent a dollar toward that deductible in 2025 when she was injured. The emergency department visit alone generated a bill of $6,200 after her insurer’s negotiated rate. Orthopedic follow-ups, imaging, occupational therapy for her wrist, and a six-week course of physical therapy brought the total billed to her insurance to just over $31,000. After her deductible and co-insurance payments, her out-of-pocket responsibility landed at approximately $22,000.

She also took six weeks of unpaid leave — her employer’s short-term disability policy had a 14-day waiting period and only covered 60% of base salary, meaning she received approximately $2,400 over the course of her leave rather than her normal $3,940 take-home for that period. The gap was roughly $1,540 she simply did not have.

Lifestyle Inflation Meets a Financial Emergency

When I asked Gladys what she would have done differently, she paused for a long time before answering. The honest answer, she said, was that the raise had made her feel invincible in a way she couldn’t fully explain until the money was gone.

Gladys covered the immediate bills through a combination of her remaining $1,100 in savings, $4,000 on a credit card, and a $7,500 personal loan she took out through her credit union at 14.9% interest. The remaining balance — approximately $9,400 — is currently in a payment plan with WakeMed’s billing department at $250 a month, interest-free for 36 months. She applied for the hospital’s financial assistance program but her annual income placed her slightly above the threshold for significant reduction.

Where Things Stand Now

As of April 2026, Gladys is back at work full-time. Her wrist has healed well enough to perform her duties, though she said cold mornings still bother her. She is paying down debt on three separate fronts simultaneously: the credit card, the personal loan, and the WakeMed payment plan. Her combined debt service on these three accounts runs approximately $680 a month.

Her appeal with the NC Industrial Commission is pending. She hired an attorney who works on contingency — meaning she pays nothing unless the appeal succeeds. Her attorney has told her the case hinges largely on the coworker’s written statement and the absence of any documented wet floor sign in the stockroom on the day of the incident. There is no guaranteed outcome.

She canceled the meal kit subscription and the gym membership the week she returned from leave. The car payment and the apartment remain. She told me she’s thought about whether to downsize, but her roommate situation is stable and moving costs money too. These are the kinds of calculations, she said, that keep her up at night now in a way they didn’t before November.

She applied for SNAP benefits during her six weeks of reduced income and was told she did not qualify at her income level, even factoring in the leave. According to the USDA’s SNAP eligibility guidelines, gross monthly income must fall at or below 130% of the federal poverty level — for a one-person household in 2025, that threshold was approximately $1,580 per month. Gladys’s reduced disability income of roughly $2,400 for the period placed her above the cutoff.

When I left the diner, Gladys walked me to my car. She seemed lighter than when we’d started talking — the way people sometimes do when they’ve said difficult things out loud to someone who isn’t already exhausted by the story. She said she hopes the appeal goes her way but has stopped counting on it. She’s building her plan around the assumption that it won’t.

That kind of recalibration — away from hope as a financial strategy — is a particular kind of hard-won clarity. Whether it arrives in time to matter is what she’s still waiting to find out.

Related: Workers Comp Denied, $22,000 in Hidden Debt Discovered — One Milwaukee Man’s Scramble for Government Benefits

Related: The Workers’ Comp Denial That Cost Aisha Jeffries More Than $14,000 — and How She’s Still Rebuilding

Leave a Reply