The most corrosive myth in American personal finance is not about investing or retirement accounts — it is the quiet, suffocating belief that accepting food assistance means you have failed. That myth, more than any income threshold or paperwork requirement, is what kept Sonia Fitzgerald from help she qualified for throughout fourteen months of genuine hardship.

I met Sonia on a cold Tuesday morning in February 2026, at a Shell station off Interstate 17 in north Phoenix. She was standing two people behind me in the prepay line, speaking in a low and strained voice into her phone. I caught fragments: they said my income was too high… but after the mortgage… and then, more quietly, please don’t tell the kids, I’ll figure it out. She hung up before she reached the register. After I paid, I introduced myself, explained what I do, and asked if she would be willing to talk. She studied me for a moment. “I’ve never told anybody,” she said. Then she agreed to coffee at the diner across the street. Two hours later, she was still talking.

The Debt That Arrived in the Mail

Sonia Fitzgerald is 34 years old and has worked as a custodian at a Phoenix Unified School District elementary school for six years. Her annual salary is approximately $27,800. She and her husband Marcus purchased a three-bedroom home in west Phoenix in 2019 for $218,000 — a decision that felt manageable, she told me, when two incomes were covering the mortgage.

Marcus died in March 2024 from a sudden cardiac event. He was 37 years old. Within six weeks of his death, Sonia began receiving collection notices on accounts she had never known existed: a Visa card with a $9,200 balance, a personal loan through an online lender for $8,400, and a joint credit card opened in both their names carrying $5,600 in revolving debt. The total came to approximately $23,200 in hidden obligations.

Because the joint credit card had been opened in both names, Sonia was legally liable for that $5,600 balance. The other accounts — opened solely in Marcus’s name — became part of his estate, but with virtually no assets to distribute, creditors continued to contact her. She spent $1,200 on a consumer debt attorney consultation just to understand what she actually owed versus what she could legally dispute.

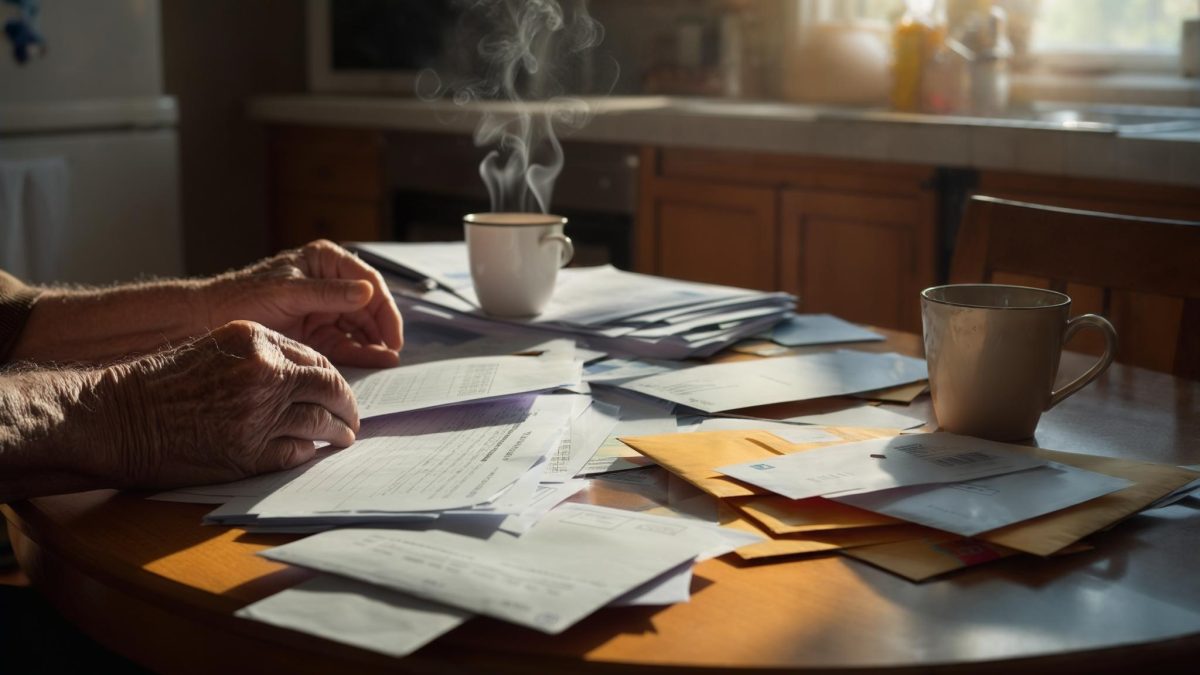

When the Mortgage Ate Everything

By mid-2024, Sonia’s take-home pay after taxes was roughly $1,940 per month. Her mortgage payment — adjusted upward after a property tax reassessment — had climbed to $1,380 a month. That left $560 for utilities, groceries, gas, car insurance, and the minimum payment on the joint credit card she had inherited.

The years when her two children were young had already erased any savings buffer. Sonia and Marcus spent between $800 and $1,100 a month on childcare during a four-year stretch in the late 2010s — costs that consumed whatever small cushion they had built. When Marcus died, there was nothing left to absorb the shock. Sonia told me she skipped meals on multiple occasions, made only minimum credit card payments, and told no one. Her two adult children, both living out of state, had no idea how serious things had become.

“They’d want to help, and they can’t afford to help,” she said. “I wasn’t going to let that happen.”

The SNAP Application She Almost Never Filed

For fourteen months, Sonia did not apply for SNAP. She had checked the income guidelines online once, seen a gross income threshold that seemed close to her salary, and concluded she didn’t qualify. She was also embarrassed. “I’m not someone who takes handouts,” she told me, then immediately paused. “I know that’s not even the right way to think about it. But that’s how it felt at the time.”

What changed was a conversation in January 2026 with a coworker who had applied for SNAP after her own divorce. The coworker walked Sonia through what the actual calculation involved. Arizona’s broad-based categorical eligibility program sets the gross income limit at approximately 200% of the federal poverty level — roughly $2,510 per month for a one-person household. Sonia’s gross monthly pay was approximately $2,317. She qualified. Not barely — she qualified with room to spare once her substantial shelter costs were applied as a deduction to her net income calculation.

Her approved monthly SNAP benefit came to $187.

Through a free tax clinic at her local library, Sonia also learned she qualified for the Earned Income Tax Credit. As a single adult with no qualifying dependents at home, her EITC for tax year 2025 came to approximately $632 — the first meaningful federal tax refund she had received in three years.

What Changed — And What Didn’t

When I followed up with Sonia in March 2026, the picture was clearer but not resolved. The $187 monthly SNAP benefit had not fixed her financial situation. She was still over-leveraged on a mortgage she could barely carry, still making minimum payments on inherited credit card debt. But the grocery assistance had freed up enough cash to stop skipping dinners.

Sonia had also connected with a HUD-approved housing counselor through the Arizona Department of Housing — a free service — who told her she may be eligible for a loan modification based on documented financial hardship. That process was still ongoing at the time this story was published.

One area she had not yet addressed: Social Security survivor benefits. Because Marcus worked and paid into Social Security, Sonia may eventually be eligible for widow’s benefits. According to SSA.gov, surviving spouses can claim as early as age 60 under current law — meaning Sonia’s eligibility window won’t open for another 26 years. Knowing that a benefit exists down the road, she told me, made her feel slightly less alone in what lies ahead.

The heaviest cost of Sonia’s situation was not the $23,200 in debt or the $1,380 mortgage. It was the fourteen months of silence — the carefully maintained fiction that everything was fine. “Nobody knew,” she told me as we wrapped up our second conversation. “And I kept thinking: if they find out, what does that say about me?” She paused for a long moment. “It doesn’t say anything about me, actually. It just happened.”

I left Phoenix thinking about how many people are having that same internal argument somewhere in America right now — at a gas station register, at a kitchen table at midnight, on a phone call they keep their voice low for. The benefits exist. The eligibility rules are wider than most people believe. The obstacle, too often, is the story we carry about who deserves to ask.

Leave a Reply