The folding table in the back of the fellowship hall at Abundant Grace Church in Tampa was set for coffee and small talk, but Pauline Thornton didn’t do small talk. She sat with her arms crossed, a paper cup going cold in front of her, and told me she almost canceled. “I don’t really do this,” she said, meaning the interview, meaning the whole conversation. “Talking about money feels like being caught with your pants down.”

Pastor Derick Howell had introduced us two weeks earlier, pulling me aside after a Wednesday service to say he knew a family going through something he thought people needed to hear about. He didn’t oversell it. He just said, “She’s proud. She’s struggling. And she finally asked for help.” That was enough for me to follow up.

A Household Budget That Was Already on the Edge

Before February 2025, Pauline Thornton’s financial life looked like a lot of lower-middle-income households in the Tampa Bay area — manageable on paper, exhausting in practice. She earns approximately $38,000 a year as an insurance claims adjuster for a regional firm in Hillsborough County. Her husband, Marcus, works part-time at a warehouse distribution center, bringing in roughly $9,600 annually. Together, their monthly net take-home was about $3,400.

Their fixed monthly obligations were relentless: $1,380 for rent on a three-bedroom in Brandon, $295 for utilities, $340 for a car payment on the vehicle Pauline needs for work. Groceries for a family of four — including a 12-year-old and a 2-year-old — ran them close to $680 a month. By Pauline’s own accounting, they had roughly $200 left at the end of each month. “There was no cushion,” she told me. “None. But we were getting by.”

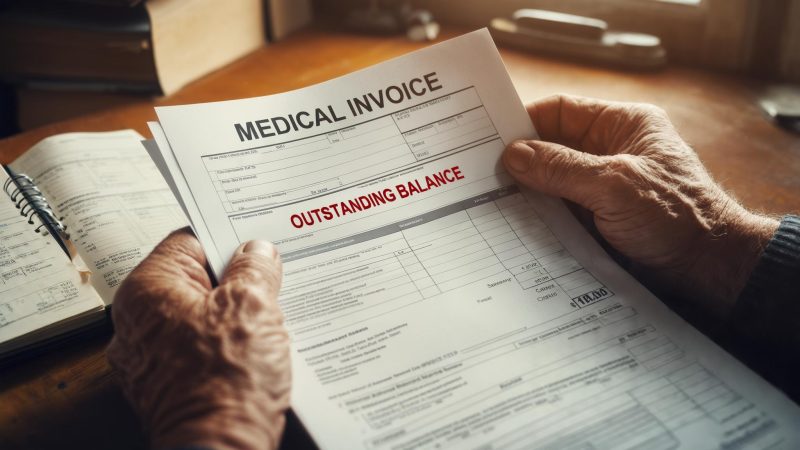

Then, in February 2025, Pauline opened a piece of mail that changed everything. It was a collections notice addressed to both of them — $27,000 across four credit cards she had never seen before, all carrying her name as a joint account holder. Marcus had been opening accounts in both their names for nearly three years, making minimum payments in secret, and watching the balances compound.

The Debt Discovery and What It Actually Did to Their Finances

Pauline described the moment with the kind of flat specificity that told me she had replayed it many times. “I sat on the kitchen floor for probably forty-five minutes,” she said. “Not crying. Just sitting. Because I already knew what the math meant.”

The math was brutal. The minimum payments on $27,000 in high-interest credit card debt came to roughly $625 a month. That amount wiped out not just their $200 buffer — it created a $425 monthly shortfall with no obvious place to cut. Marcus reduced his hours further during the fallout of the confrontation, dropping their combined income by another $280 a month through March.

Groceries became the first thing to compress. Pauline told me she cut the family food budget from $680 to $310 in March 2025, subsisting heavily on rice, canned goods, and a neighbor’s garden surplus. Her 2-year-old was eating well enough, she said, but she noticed her 12-year-old coming home hungry after school lunches that weren’t covering it. “That was the line,” she said. “When I saw that, I called the number.”

Applying for SNAP — and Everything That Made It Harder Than It Should Have Been

Pauline had never applied for a government benefits program in her life. She described her upbringing — her mother worked two jobs, never took assistance, and treated it as a point of honor. That worldview had calcified into something close to shame. “I genuinely believed SNAP was for people who weren’t trying,” she told me, without apology. “I know how that sounds. But that’s what I thought.”

She applied through Florida’s ACCESS system online in early April 2025. According to USDA Food and Nutrition Service, SNAP eligibility for most households requires gross monthly income at or below 130% of the federal poverty level — for a family of four in 2025, that threshold was approximately $3,473 per month. With Pauline’s reduced combined household income that month sitting near $3,100, they qualified on paper.

The application itself took Pauline three attempts. The first time, she didn’t have Marcus’s pay stubs from his part-time employer. The second time, the system timed out before she could upload documents. On the third attempt, in mid-April, she completed it — but the interview required by the state wasn’t scheduled until May 7th, more than three weeks later. That wait, she told me, felt like the longest of her life.

- April 3, 2025: Initial application submitted through Florida ACCESS

- April 3–7: Document gathering (pay stubs, lease agreement, ID)

- Two failed upload attempts due to system errors

- April 14: Completed application accepted

- May 7: Phone interview conducted with DCF eligibility specialist

- May 12: Approval notice received; EBT card mailed

What the Benefits Actually Covered — and What They Didn’t

Pauline’s household was approved for $522 per month in SNAP benefits beginning in May 2025. She called it “a relief and an embarrassment at the same time,” and she said that without hesitation, as if the two feelings had learned to coexist.

The $522 covered most of the family’s food needs when combined with the $310 she was still budgeting from her paycheck. Her 2-year-old was also enrolled in Florida Healthy Kids for health coverage — a step Pauline had taken right after the baby was born, one of the few times she’d accepted help before this crisis. But prescription costs for Marcus, who needed medication for a back injury sustained at work in 2023, were still coming out of pocket: $94 a month that the family had no clean answer for.

The SNAP benefit resolved the most visible crisis — the kids were eating well again. But the structural problem, $27,000 in debt accruing interest, remained entirely unsolved. Pauline’s credit score dropped 94 points between February and June 2025 as she missed a payment during the chaos of the initial discovery. The family hadn’t yet consulted a nonprofit credit counseling service, though Pastor Howell had mentioned one to her.

Where Things Stand Now — and What Pauline Wants Other People to Know

When I spoke with Pauline in late March 2026, she had been receiving SNAP for just under a year. Her benefit had been recertified in November 2025, dropping slightly to $498 per month after Marcus picked up additional hours. She was not upset about the reduction — she called it “a sign things are moving, even if slowly.”

The debt remains. She and Marcus have entered a repayment plan through a nonprofit credit counseling organization — something she only agreed to, she admitted, because Pastor Howell printed out their number and left it in her car without comment. The marriage is strained but intact. Pauline described the trust situation as “a renovation project that doesn’t have a completion date.”

What struck me most about Pauline wasn’t her pride or her stubbornness — it was her precision. She knew every number in her household. She knew the exact benefit reduction amount to the dollar. She knew what her credit score was the day I interviewed her (641, she said, without being asked). This was not someone who lacked financial literacy. This was someone who had been dealt a problem she hadn’t created and was managing it the only way she knew how: by tracking it obsessively.

When I asked what she wished she had known before all of this, she was quiet for a moment. Then she said something that I’ve thought about since: “I thought SNAP was giving up. But it turns out it was just — a thing that existed. A thing I needed. Those aren’t the same.”

I left that fellowship hall thinking about the distance between what people believe about government assistance and what it actually looks like in practice — a woman at a folding table, a cold cup of coffee, and a precise accounting of every dollar her family had spent and lost and scraped back together. Pauline Thornton didn’t become a different person when she applied for SNAP. She just became someone who had run out of other options, and chose her kids over her pride. That’s not a cautionary tale. It’s just what happened.

Related: She Filed for Social Security at 67 — Then Learned Her Graduate School Debt Could Still Follow Her Into Retirement

Related: A Social Worker Who Spent His Career Helping Others Found Himself Drowning in Debt — Until One Tax Credit Changed His Math

Leave a Reply