She turned 65 in early April, assumed her Medicare paperwork would sort itself out after she retired, and didn’t get around to enrolling in Part B until late summer. That was 30 days past the deadline. The penalty notice arrived quietly; a small percentage added to her monthly premium, and she almost didn’t notice it until her financial advisor ran the numbers.

That small percentage translates to roughly $2,000 in extra premiums over the first decade, with the meter still running for as long as she holds Part B coverage. Thirty days late. Permanent consequence.

This isn’t a rare edge case. Medicare’s enrollment windows are rigid, the penalty is lifelong, and the rules are far less intuitive than Social Security or employer benefits. Here’s what actually happens when you miss that window; and what your options are if you already have.

What Most People Assume About Medicare Enrollment

The dominant assumption is that Medicare enrollment works roughly like signing up for a streaming service: you miss the window, you pay a small fee, you move on. Many people also assume Medicare starts automatically at 65, the way Social Security benefits can be configured to begin without active enrollment.

Neither assumption is correct. Medicare Part B, which covers outpatient care, doctor visits, and preventive services; is not automatic for most people, according to firstpersonfinance.com. You have to actively enroll.

And if you miss your Initial Enrollment Period (IEP) without having qualifying coverage elsewhere, the penalty that follows isn’t a one-time fine. It compounds annually and stays with you permanently.

A second common belief is that the General Enrollment Period (January 1 through March 31 each year) functions as a penalty-free do-over. It doesn’t. Enrolling during the General Enrollment Period after missing your IEP still triggers the late penalty in most cases, unless you qualify for a Special Enrollment Period.

How the Medicare Part B Enrollment Window Actually Works

Your Initial Enrollment Period spans seven months: three months before the month you turn 65, the month of your birthday, and three months after. Miss that window without having qualifying employer-sponsored coverage, and you’ve triggered the penalty clock.

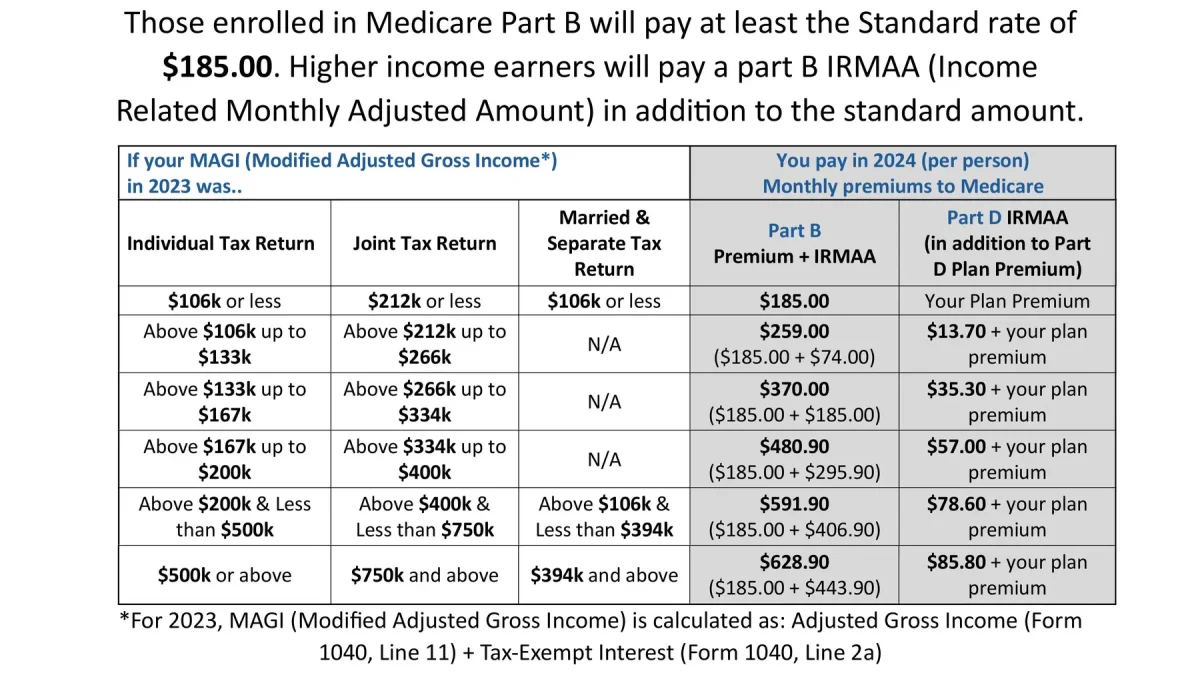

For every full 12-month period you go without Part B when you were eligible, your premium increases by 10%. That penalty is calculated on top of the standard monthly premium; which stands at $185.00 per month as of 2026. One year of delay adds $18.50 per month.

Two years adds $37.00. The math is straightforward, but the long-term cost is anything but small.

| Years Delayed | Penalty % | Monthly Surcharge (2026) | Extra Cost Over 10 Years |

|---|---|---|---|

| 1 year | 10% | +$18.50 | ~$2,220 |

| 2 years | 20% | +$37.00 | ~$4,440 |

| 3 years | 30% | +$55.50 | ~$6,660 |

| 4 years | 40% | +$74.00 | ~$8,880 |

Note that these figures use the flat 2026 premium. With even modest annual premium growth of 3%, the real 10-year cost of a one-year delay climbs closer to $2,600. Over 20 years, it can exceed $5,900 for a single missed year. According to Medicare Interactive, this penalty applies for as long as you have Part B, there is no point at which it expires or resets.

Missed Medicare Open Enrollment? Here Are Your Actual Options

If you’ve already missed your Initial Enrollment Period, your path forward depends on why you missed it and what coverage you had in the meantime.

Option 1: Special Enrollment Period (SEP). If you were covered by an employer-sponsored group health plan through your own or a spouse’s active employment, you qualify for a Special Enrollment Period. You can enroll in Part B during the SEP without triggering the late penalty. According to KFF, the SEP lasts for eight months after your employment or employer coverage ends; whichever comes first. This is the one legitimate escape hatch from the penalty.

Option 2: General Enrollment Period. If you don’t qualify for an SEP, you must wait for the General Enrollment Period, which runs January 1 through March 31 each year. Coverage begins July 1 of that year. The late penalty will apply. As UnitedHealthcare notes, this is a fallback, not a workaround.

- SEP enrollment: no penalty, coverage begins the month after you enroll

- General Enrollment Period: penalty applies, coverage delayed until July 1

- No enrollment at all: you remain uninsured for Part B services until you act

Option 3: Appeal or Equitable Relief. In rare cases; typically involving documented misinformation from a federal agency, Medicare beneficiaries have successfully appealed late penalties. This process is difficult, slow, and not guaranteed. It requires written documentation and is handled on a case-by-case basis.

Why the 30-Day Mistake Carries a Permanent Price Tag

The scenario in the headline, missing the window by just 30 days; is more common than Medicare’s official communications suggest. The seven-month IEP sounds generous, but it’s easy to miscalculate. Many people count from their birthday rather than the month before it.

Others assume their HR department will handle the transition. Some simply don’t know the window exists.

Thirty days past the deadline means you’ve missed the IEP entirely. Medicare doesn’t distinguish between someone who was 30 days late and someone who was 11 months late, both trigger the same 10% penalty per full 12-month period of delay. The penalty is calculated based on how many full years you went without Part B when you were eligible, not on how late you enrolled within a given year.

“For as long as they have Medicare, they must pay their monthly Part B premium plus an additional 10% for each year they delayed signing up.”; Medicare Rights Center

At the 2026 standard premium of $185.00/month, a 10% penalty adds $18.50 per month, $222 per year. Over ten years, that’s $2,220 in extra payments, assuming premiums never rise. With realistic annual increases, the decade total is closer to $2,600 to $2,800. That’s what a 30-day mistake costs in practical terms.

What This Means for Anyone Approaching 65

The practical implication is simple: treat your Medicare enrollment window like a legal deadline, not a suggestion. Mark the first day of the month three months before your 65th birthday as your enrollment start date. Don’t wait for a notice in the mail — Social Security doesn’t always send reminders, and the absence of a warning letter is not a grace period.

If you’re still working at 65 and covered by a qualifying employer plan, document that coverage carefully. When you do eventually retire, you’ll need proof of that coverage to claim your Special Enrollment Period and avoid the penalty. Keep explanation of benefits statements, employer coverage letters, or HR confirmation emails.

- Enroll online at SSA.gov up to three months before your 65th birthday

- If you’re already receiving Social Security benefits, Part A enrollment is usually automatic — but Part B requires a separate decision

- Contact your State Health Insurance Assistance Program (SHIP) for free, unbiased counseling — every state has one

- If you missed the window and don’t qualify for an SEP, enroll during the next General Enrollment Period (January 1–March 31) to stop the penalty from growing

The Medicare Annual Enrollment Period, which ends December 7 each year, is primarily for changing existing Medicare Advantage or Part D drug plans — not for first-time Part B enrollment. These periods serve different purposes, and confusing them is another common source of costly mistakes.

Missing your Medicare Part B window by 30 days doesn’t feel catastrophic in the moment. The penalty is quiet, automatic, and permanent. By the time most people notice it, they’ve already paid hundreds of dollars they didn’t have to.

The enrollment calendar is unforgiving — but it’s also entirely knowable in advance. That’s the part worth acting on now, before the window closes.

More Stories Like This

- The Medicare Part B Enrollment Deadline Most New Retirees Never Hear About — Missing It by 3 Months Still Cost Me $2,000 in Penalties

- She Assumed Medicare Started Automatically at 65 — That 30-Day Mistake Now Costs Her $3,000 and Counting (firstpersonfinance.com)

- The Medicare Appeals Process That Reversed a $180,000 Surgery Denial Exists for Every Beneficiary — Most Patients Never Learn It's an Option, according to firstpersonfinance.com

Frequently Asked Questions

Leave a Reply