With three years until his target retirement date, Warren Jeffries is not the kind of man who leaves things to chance. When I sat down with the 62-year-old IT project manager at a coffee shop in Raleigh, North Carolina, in late March 2026, he pulled out a printed spreadsheet before we had even ordered. He had color-coded rows for projected withdrawals, Medicare start dates, and estimated Social Security income under three different claiming scenarios.

He has $680,000 in retirement accounts. His home is paid off. By most measures, he is well ahead of the average American approaching retirement. Yet Warren told me, almost immediately, that he hadn’t slept well in months.

“I’ve done the spreadsheets,” he said, smoothing the paper in front of him. “I know what the numbers say. But I can’t make myself believe it’s going to be fine.”

A Position That Looks Comfortable From the Outside

Warren spent 28 years in IT project management, mostly for mid-size healthcare companies in the Research Triangle. His wife, Carol, 60, works part-time as a dental hygienist and plans to retire around the same time. Together, they contributed steadily to 401(k) accounts, reinvested dividends, and made the decision 11 years ago to accelerate their mortgage payments — a choice Warren credits with giving them more flexibility now.

On paper, the picture is solid. A $680,000 portfolio, a paid-off home in a lower-cost city, and Social Security income that — depending on when they claim — could provide a meaningful monthly floor. But Warren describes himself as a “worst-case scenario thinker,” and when I asked him to walk me through his concerns, the list was specific and sequenced.

His first concern is longevity. If Warren retires at 65 and lives to 92 — a realistic scenario given family history on both sides — his savings need to last 27 years, and Carol’s slightly longer. Using a commonly referenced 4% annual withdrawal guideline, $680,000 would generate roughly $27,200 per year before Social Security income begins. That number feels thin to Warren, especially with two people and no employer-sponsored health coverage on the horizon.

The Healthcare Gap He Didn’t Fully Account For

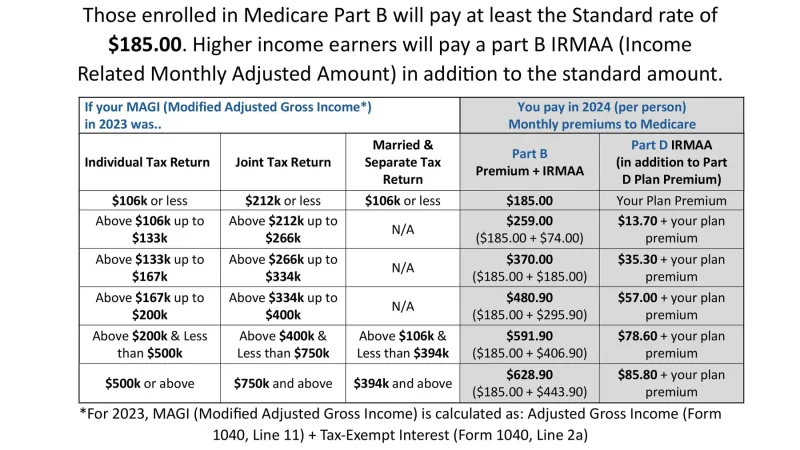

Here is where Warren’s planning hits a concrete wall. Medicare eligibility begins at age 65 for most Americans, according to Medicare.gov. Warren turns 65 in three years and would qualify right at retirement. Carol, however, is two years younger. If they retire together, she faces a two-year window with no employer insurance and no Medicare coverage.

“Carol is two years younger than me,” Warren told me, leaning forward in his chair. “So even if I hit Medicare at 65, she’s got a two-year gap we have to cover. I looked at ACA marketplace plans for her age range in North Carolina. We’re talking somewhere around $900 to $1,100 a month just for her, depending on the plan.”

That gap — approximately $21,600 to $26,400 over two years — isn’t catastrophic on its own. But it compounds against every other variable Warren is tracking.

Warren had initially assumed Carol could continue on his employer coverage through COBRA after he retired, but COBRA continuation coverage typically lasts only 18 months and requires the individual to pay the full premium — including the portion previously covered by the employer. For a couple planning a multi-decade retirement, it functions as a bridge at best, not a long-term solution.

The Phone Call That Comes Every Month

Warren has a 32-year-old son, Marcus, who launched a home renovation business in 2022. By late 2024, the business had failed — a combination of cost overruns, a slowing housing market, and a dispute with a contractor that ended in a lawsuit. Marcus is rebuilding now, working a salaried job, but he carries significant debt from the venture and calls his father most months asking for help.

Warren has given him money. He wouldn’t specify the total to me, describing it only as “enough to matter on a spreadsheet.” He estimates the requests come in amounts between $500 and $2,000, roughly every six to eight weeks. Over the past year, he calculates he has transferred somewhere between $8,000 and $10,000 to Marcus.

“Every time my son calls, I want to help him,” Warren told me. “He’s my kid. But at some point I have to ask — at whose expense?”

It is a question Warren has not yet answered to his own satisfaction. He and Carol have had the conversation more than once, and they don’t fully agree. Carol is more inclined to help Marcus short-term. Warren sees every dollar given as a dollar that is no longer compounding in their retirement accounts over the next three years.

The Social Security Decision He Keeps Circling Back To

Warren’s full retirement age for Social Security is 67, as it is for most Americans born in 1964, according to the Social Security Administration. If he retires at 65 and claims immediately, he receives a reduced benefit — roughly 13% less than his full amount. If he waits until 67, he collects his full benefit. If he delays until 70, his monthly payment grows by approximately 8% per year beyond full retirement age.

Over a 30-year retirement, that spread is not trivial. Warren has been modeling all three scenarios, and the comparison is doing nothing to calm his nerves.

Warren has been leaning toward claiming at 65, mostly because he doesn’t want to draw down his portfolio for two additional years while waiting for his full retirement age. But he hasn’t committed. “Three years feels like a long time until you realize it’s not,” he told me, staring briefly at the table in front of him.

Where Warren Stands Now — and What He Has Actually Changed

By the time we finished talking, Warren had described a situation with no clean resolution. He and Carol have not cut off Marcus — and Warren doesn’t sound like he will. But he told me he had recently had a direct conversation with his son, the first one in which he laid out specific numbers: what he and Carol have saved, what they need it to last, and what the monthly support is costing them in compounding returns over three years.

“Marcus didn’t know any of that,” Warren said. “I think he thought we were fine. We are fine — but not infinitely fine.”

On the healthcare side, Warren told me Carol had agreed to look at what ACA marketplace options would actually cost in North Carolina for her age. They are also exploring whether she might work part-time for another year or two after Warren retires, both for income and to maintain employer-sponsored health coverage a bit longer before her own Medicare eligibility begins.

Warren hasn’t resolved his anxiety. When I asked him directly whether he felt more at peace after working through all of this, he laughed quietly. “I feel more organized,” he said. “That’s not the same thing.”

What struck me about Warren Jeffries isn’t that he’s struggling — by most retirement benchmarks, he isn’t. What struck me is that the anxieties he carries are not irrational. The healthcare gap is real. The Social Security tradeoff is real. The slow drain of family support over time is real. The variables that keep him up at night are the ones no spreadsheet can fully predict: market returns, medical costs, how long two people will live, and whether a son’s next chapter will require more help or none at all.

He folded his spreadsheet carefully before standing to leave. At the door, he paused and said something I keep coming back to: “The math isn’t the hard part. The hard part is trusting the math when everything else feels uncertain.”

Related: A Denver Nurse Paying $1,400 a Month for Daycare Didn’t Know She Qualified for a $2,000 Tax Credit

Leave a Reply