Conventional wisdom says that claiming Social Security the moment you’re eligible is a sign of financial desperation — a last resort for people who failed to plan. But after spending weeks corresponding with Brittany Bianchi, a 66-year-old bank teller from Oklahoma City, I came to believe that desperation and practicality can look identical from the outside, and that the real story is almost always more complicated than the decision itself.

I first encountered Brittany through a comment she left on a previous article I’d written about co-signing risks and retirement security. Her comment was brief — just three sentences — but it stopped me cold. She wrote that she had co-signed a personal loan for a close friend in 2021, that the friend had stopped making payments by early 2023, and that the fallout had changed nearly every financial calculation she’d made for her sixties. I reached out the same afternoon. She agreed to talk two days later.

The Loan That Changed Everything

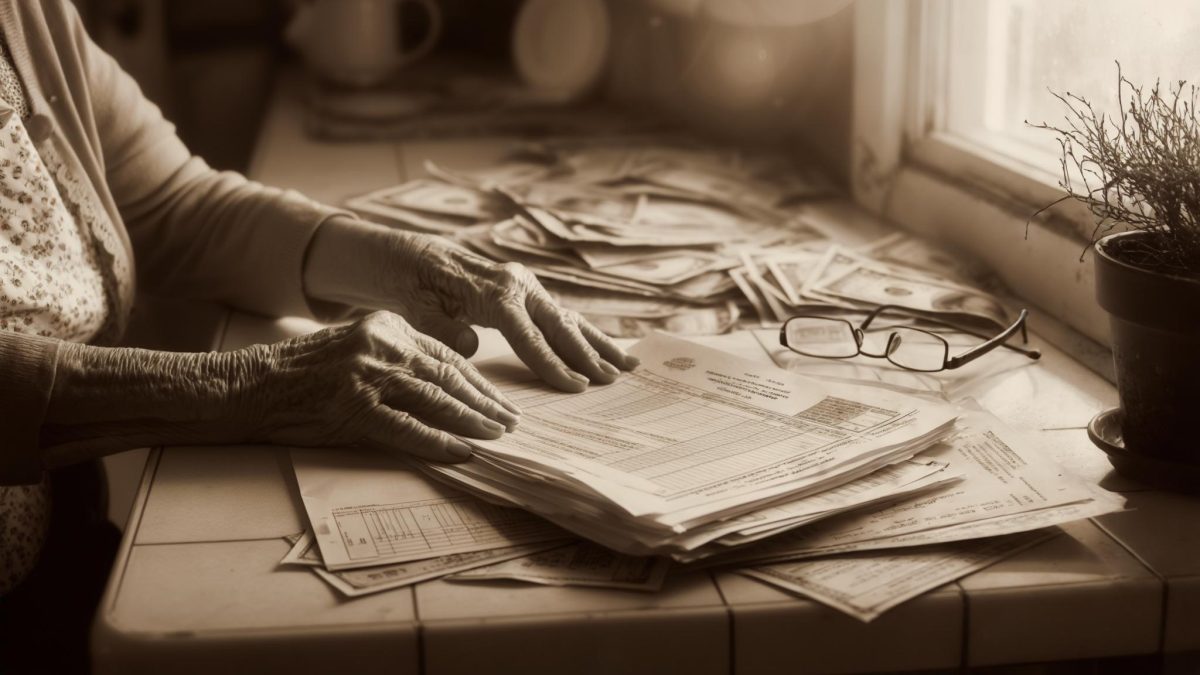

When I sat down with Brittany Bianchi over a video call on a Tuesday morning in late February, she had just finished her shift at the bank and was still in her work lanyard. She looked tired in the precise way that people do when they’ve been tired for a long time and have stopped noticing it.

The co-signed loan, she told me, was for $18,500 — a personal loan her longtime friend Denise took out to cover a gap between jobs and a car repair. Brittany had known Denise for over twenty years. “She’d always paid me back before,” Brittany told me. “It was never a question in my mind.” Denise made payments for about fourteen months before they stopped completely in March 2023. By the time the lender contacted Brittany, the outstanding balance had grown to roughly $15,200 with interest and fees.

Brittany’s credit score, which had been hovering around 710, dropped to 581 within two billing cycles. The account showed as delinquent on her report. Refinancing anything became difficult. A small landscaping and outdoor cleaning business she’d been running on weekends — which had brought in around $1,100 to $1,400 a month at its peak in 2021 and 2022 — was already losing customers to cheaper competitors. The combination of lost side income and a damaged credit profile left her with very little cushion.

Her husband Marcus works part-time at a hardware store and brings home roughly $1,050 a month. They have two children together — a six-year-old and a four-year-old — which surprises people when they learn Brittany’s age, and which she acknowledges with a quiet, dry humor. “People do the math and they give me this look,” she said. “I see it all the time at the bank.” The children are the reason, she told me, that she simply cannot afford to coast.

The Social Security Decision She Made Under Pressure

Brittany turned 66 in September 2025. At that age, she was not yet at her full retirement age under Social Security rules — that threshold, for people born in 1959, falls at 66 years and 10 months. But she began seriously researching her options after the co-sign default wiped out what had been a modest emergency fund.

She did not claim immediately at 66. Instead, she spent several months running numbers, reading SSA materials, and — she admitted — lying awake at night. She finally filed in January 2026, roughly nine months before reaching her full retirement age. Her monthly benefit came out to approximately $1,340, reduced from what she would have received at full retirement age. Had she waited until 70, according to Kiplinger’s analysis of maximum Social Security payments, the top benefit for someone delaying to 70 can reach $5,181 per month — though that figure depends on a lifetime of maximum earnings. Brittany’s number was never going to be that high. But the gap between what she’s collecting now and what she could have collected at full retirement age still stings.

“I knew it wasn’t the ‘right’ time on paper,” Brittany told me. “But paper doesn’t pay for groceries.” She still works full-time at the bank — her annual salary is approximately $34,000 — and the Social Security income was meant to help cover the $15,200 debt she’d been making minimum payments on. It was not supposed to be her primary income. It became a patch on a leak she hadn’t expected to have.

When the COLA Raise Arrived — and Then Mostly Left

Social Security beneficiaries received a 2.8% cost-of-living adjustment for 2026, according to CNBC’s reporting on COLA estimates. For Brittany, that 2.8% bump translated to roughly $37 more per month on her benefit. It felt meaningful when she first read the notice.

Then she saw the Medicare Part B premium figure. The standard premium rose to $202.90 per month in 2026, up $17.90 — a 9.7% increase — from the $185 monthly rate in 2025, as Business Insider’s Social Security 2026 overview noted. Because Medicare Part B premiums are typically deducted directly from Social Security checks, Brittany’s net increase from the COLA was almost entirely absorbed by the premium hike. She calculated the difference herself, in pencil, on a notepad she keeps by the kitchen phone.

“The raise was thirty-seven dollars. The Medicare went up almost eighteen,” she said. “So I got maybe twenty dollars extra. Which — fine. But I’d been counting on that raise for months.”

This pattern — COLA giveth, Medicare taketh — is not unique to Brittany. As reporting on the 2026 COLA’s net impact found, many beneficiaries saw Medicare premiums consume the majority of their raise. For lower-benefit recipients like Brittany, whose check is already reduced due to early claiming, the math is especially unforgiving.

The Business She Built and the Business She’s Losing

Before the financial cascade of 2023, Brittany had felt genuinely optimistic about her side business. She’d started it in 2019, during a slow stretch at the bank, offering pressure washing and basic landscaping to residential customers in her neighborhood. At its peak it served about eleven regular clients. By the fall of 2024, she was down to four.

She attributes the decline partly to competition from younger operators with newer equipment, and partly to the reality that she simply couldn’t invest in marketing or tools while also managing the debt from the co-signed loan. The business brought in approximately $410 in her best month of 2025 — down from that $1,100 to $1,400 monthly average three years earlier. She hasn’t formally closed it, but she describes it in the past tense without seeming to notice.

She hasn’t told her siblings about the loan default or the business decline. Her mother is in her late eighties and lives in Tulsa; Brittany sends her $200 a month when she can. Asking for help, she made clear without quite saying it directly, is not something she knows how to do. “We figure it out,” she said, twice, in slightly different ways.

Where Things Stand Now — and What She’s Watching

As of March 2026, Brittany is bringing in roughly $3,590 a month combined: her bank salary net of taxes, Social Security after the Medicare deduction, and the reduced side-business income. Her household expenses — mortgage, utilities, groceries, childcare for the four-year-old, and debt payments — come to approximately $3,410. She has about $180 of margin in a typical month. There is no emergency fund.

She told me she checks the Medicare.gov account portal periodically to track her coverage and costs, something she started doing only after the 2026 premium increase caught her off guard. “I didn’t know they’d go up that much,” she said. “I should have looked earlier.”

She’s aware that early COLA projections for 2027 are trending lower than 2026’s 2.8% boost. She’s also aware — in the general way that people who can’t afford to dwell on bad news are aware — that the Congressional Budget Office has projected that Social Security benefit reductions could begin as early as 2040 if the program’s financing shortfall isn’t addressed. She doesn’t have twenty years of runway to wait and see what happens to the program. Her youngest child will be in high school by then.

What struck me most in our conversations — we spoke three times over the course of a month — was how clearly Brittany understood the trade-offs she’d made and how little she allowed herself to feel sorry about them. She filed for benefits nine months before her full retirement age, knowing it would reduce her monthly check permanently. She did it because the alternative was worse. That’s not a failure of financial planning. It’s what financial pressure actually looks like from the inside.

When I asked what she’d tell someone facing the same choice, she was quiet for a moment. Then: “I’d tell them to read everything before they sign anything. I’d tell them that.” She meant the loan, not the Social Security form. She’s still paying for the loan. She’ll be collecting the reduced Social Security check for the rest of her life.

Related: He Got a Raise and Thought He Was Set — Then the IRS Bill Arrived and His Retirement Math Fell Apart

Leave a Reply