Have you ever avoided opening your own mail because you were afraid of what was inside? Carlos Becerra, 61, told me he went six weeks without checking his bank statements after his workers’ compensation claim was denied. Not because he didn’t care — because he cared too much and couldn’t absorb one more number going the wrong direction.

I found Carlos in February 2026 through a Facebook group for retirees and pre-retirees in the Greater Cleveland area. He’d posted a short, plainspoken comment about his workers’ comp denial that caught my eye: “They said I had a pre-existing condition. My back was fine until I hit that concrete floor.” I sent him a direct message. He responded within the hour. We met over coffee in Cleveland’s Old Brooklyn neighborhood three days later, and he talked for nearly two hours.

What he described wasn’t one crisis — it was three, hitting in rapid sequence, with no financial cushion between them.

The Fall That Started Everything

On October 14, 2024, Carlos was on a commercial job site near downtown Cleveland when scaffolding shifted and he dropped roughly eight feet onto a concrete sub-floor. He landed on his back and left shoulder. An ambulance took him to MetroHealth Medical Center, where imaging showed two herniated discs in his lumbar spine and a partial rotator cuff tear.

He spent four days inpatient and was told he could not return to electrical work for a minimum of twelve weeks. His union’s short-term disability policy activated at roughly $1,400 a month — about half of his typical take-home pay of $2,840. That gap mattered immediately.

His fixed monthly obligations were already tight. Rent on his one-bedroom apartment in Old Brooklyn ran $875 a month. Child support for his two kids — a 14-year-old daughter and a 16-year-old son from his marriage that ended in 2019 — totaled $580 monthly, a figure set by the court when he was earning full wages. After the injury, those same obligations now consumed nearly 105% of his disability income before utilities, food, or transportation.

“The math doesn’t work,” Carlos told me, stirring his coffee without drinking it. “I kept thinking someone would fix it. The union, the insurance, the workers’ comp. Someone. But everybody had a reason it wasn’t their problem.”

When Workers’ Comp Said No

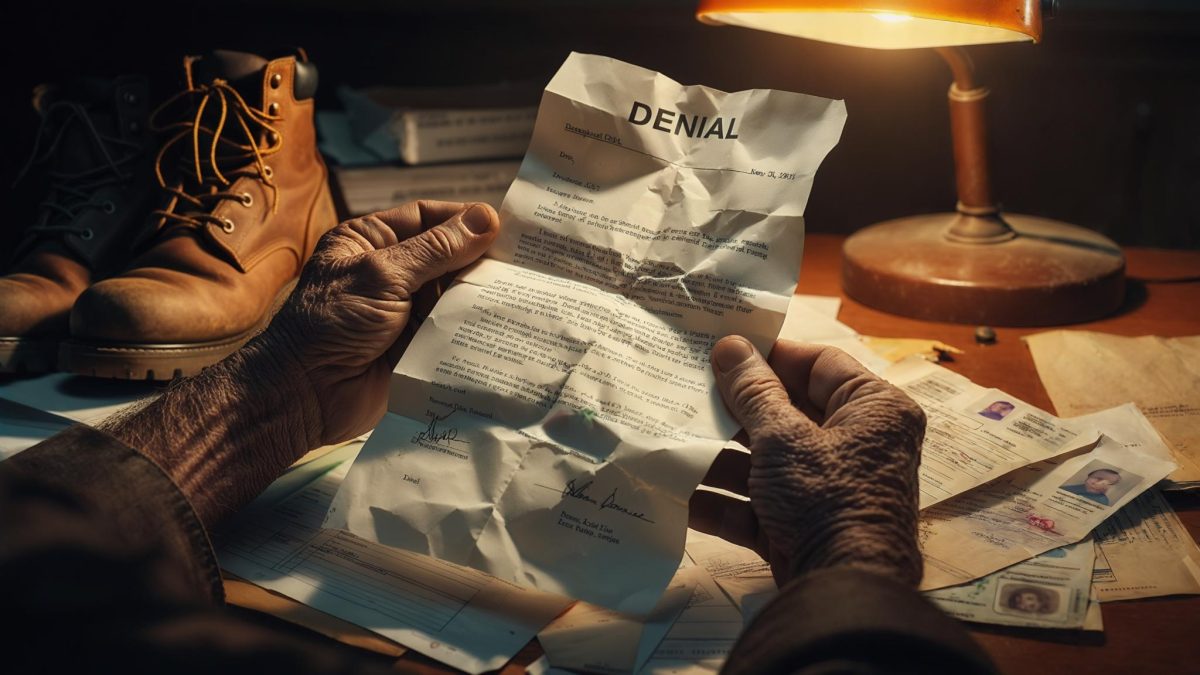

Ohio’s workers’ compensation system, administered through the Ohio Bureau of Workers’ Compensation, generally covers injuries sustained on the job — including falls from scaffolding. But claims can be denied when employers or their insurers argue that a condition was pre-existing or that the workplace wasn’t the proximate cause of injury.

Carlos received his denial letter on February 7, 2025. The reason stated: the insurer argued his lumbar issues were consistent with degenerative disc disease predating the fall. He had, in fact, seen a chiropractor twice in 2022 for lower back stiffness. That two-year-old chiropractic record became the pivot point of the denial.

Carlos told me he didn’t know he could appeal. His union steward mentioned it offhandedly three weeks after the deadline had passed. By then, the window for the initial appeal had closed. He was left with approximately $14,200 in out-of-pocket medical expenses — the portion his union health insurance did not cover — and no workers’ comp settlement to offset it.

He explored hiring a workers’ comp attorney on contingency. One attorney told him that, with the appeal window closed and the documentation as it stood, the case was difficult — not impossible, but expensive to pursue. Carlos decided he couldn’t take on more uncertainty.

The Identity Theft He Didn’t See Coming

In March 2025, Carlos attempted to take out a small personal loan to cover a portion of his medical debt. When the lender pulled his credit, they found something unexpected: his credit score had dropped from approximately 680 to 512. There were four accounts on his report he had never opened — two credit cards, a retail store line of credit, and a personal loan — totaling roughly $23,000 in fraudulent debt.

According to the Federal Trade Commission’s identity theft resources, victims should file a report at IdentityTheft.gov immediately and place a free fraud alert or credit freeze with all three major bureaus. Carlos did not know these steps existed when he first discovered the fraud.

Carlos spent roughly six weeks working through the dispute process with each bureau. He filed a police report with the Cleveland Division of Police. He submitted an FTC identity theft report. He placed freezes on all three bureaus. But the fraudulent accounts remained in dispute for months, and while they were under investigation, his borrowing options effectively disappeared.

“I felt like someone had reached into my wallet and taken my whole future,” Carlos said. “Not cash — my whole future. My ability to borrow, my ability to rent a different apartment someday, my ability to do anything. It was all just gone.”

Applying for SNAP — and What That Process Was Like

By April 2025, Carlos’s monthly budget looked like this:

- Short-term disability income: $1,400/month

- Rent: $875/month

- Child support: $580/month

- Utilities (gas, electric, internet): approximately $210/month

- Transportation: $85/month (bus pass and occasional rideshare)

- Remaining for food, medication, and everything else: negative $350/month

A neighbor who worked at a community health center told Carlos he might qualify for SNAP — the Supplemental Nutrition Assistance Program — based on his current income and household size of one. He was skeptical. “I always thought SNAP was for people who were really in trouble,” he told me. “I didn’t think of myself that way. But I guess I was.”

The $291 a month didn’t solve his deficit. But it meant he could eat without going further into debt on a credit card — credit he could barely access anyway, given the identity theft damage. “That card probably kept me from doing something stupid with what little credit I had left,” he told me.

Where Things Stand — and What He’s Still Figuring Out

When I spoke with Carlos in early 2026, he had returned to partial work — light electrical tasks that don’t require heavy lifting or extended time on ladders. His take-home had climbed back to roughly $1,950 a month, but his SNAP benefit was reduced accordingly when he reported the income change, dropping to $187 a month.

His credit score had recovered to approximately 588 after the fraudulent accounts were removed — still low enough to limit his options, but no longer in freefall. The child support obligation remains unchanged; he’s exploring whether a modification petition makes sense given the documented income disruption, but he hasn’t filed anything yet.

He’s also begun looking into Social Security Disability Insurance. According to the Social Security Administration, SSDI eligibility requires a medical condition that prevents substantial gainful activity for at least 12 months and sufficient work history. Carlos has the work history — over 30 years of union contributions — but his doctors have not yet certified that his back condition meets the SSA’s definition of a disabling impairment. That process is ongoing.

That anger, he was quick to add, hasn’t curdled into hopelessness. He still calls himself an optimist. He showed me a photo on his phone of his son’s high school track meet from last fall — Carlos in the bleachers, grinning, wearing a back brace under his jacket. He’d driven forty minutes each way to get there.

What struck me sitting across from Carlos wasn’t the scale of what went wrong. It was the speed. One fall in October 2024. A denial letter in February 2025. A stolen identity discovered in March 2025. Four months — and a man with thirty years of union work behind him was applying for food assistance and learning what a credit freeze was for the first time.

He told me something at the end of our conversation that I’ve thought about since: “I used to think the safety net was for people who made mistakes. Now I think it’s for people who got unlucky. I didn’t do anything wrong. I just fell.”

Related: Workers Comp Denied, $22,000 in Hidden Debt Discovered — One Milwaukee Man’s Scramble for Government Benefits

Related: She Was 67 and Still Working Full-Time — Then a Credit Union Manager Told Her She’d Been Missing a Key Tax Credit for Years

Leave a Reply