Roughly one in four families who lose SNAP eligibility after an income increase end up spending more on basic necessities than the wage gain actually covers — a trap that economists call the benefits cliff. That statistic lived as an abstraction to me until a Tuesday afternoon in February 2025, when I found myself sitting next to Benny Valdez in the plastic-chair waiting room of the Atlanta Social Security Administration field office on Peachtree Street.

I was there reporting a different story entirely — a piece on delayed survivor benefit applications. Benny was there trying to sort out a discrepancy in his earnings record. We got to talking, the way strangers do when the wait is long and the fluorescent lights are unforgiving. By the time his number was called, I had asked if he would let me tell his story. He said yes without hesitating.

A Blended Family, a Startup Salary, and a Budget That Never Quite Balanced

Benny Valdez is 31, analytical in the way people get when they have had to be — he tracks every expense in a spreadsheet he built himself, color-coded by category. He has been a marketing manager at a small Atlanta-based SaaS startup since March 2023, earning what he described to me as “a respectable title and a not-so-respectable paycheck.” His base salary when he was hired was $42,000 a year.

He and his wife Daria, 33, have three children between them from previous relationships — his daughter Maya, 8, Daria’s twin boys Elliot and Marcus, 6. The household of five runs on two incomes, though Daria’s work as a part-time dental receptionist brings in inconsistent hours. Some months she clears $1,400. Other months, when shifts are cut, she clears $800.

That irregularity is its own kind of tax. “I can’t budget to a number that changes every month,” Benny told me when we sat down for a longer conversation the following week at a coffee shop near his home in Decatur. “So I budget to the worst case, and we just live lean when it turns out better.”

For much of 2023 and 2024, the family qualified for SNAP benefits. With a household of five and a combined gross income hovering around $3,500 a month — below the 130 percent federal poverty threshold that governs SNAP eligibility — they were receiving approximately $612 per month in food assistance, according to Benny’s records. That money, he told me, was the difference between making rent and not making rent in months when Daria’s hours dropped.

The Raise That Changed Everything — and Not in the Way He Expected

In September 2024, Benny’s startup completed a small Series A funding round. Two weeks later, his manager called him into a conference room and told him the company was bumping his salary to $51,000, effective October 1. It was, by any reasonable measure, good news. A $9,000 annual increase. He called Daria from the parking garage.

“I genuinely thought we had turned a corner,” he told me. “I was doing the math in my head — that’s like $750 more a month before taxes. We could finally build up the emergency fund.”

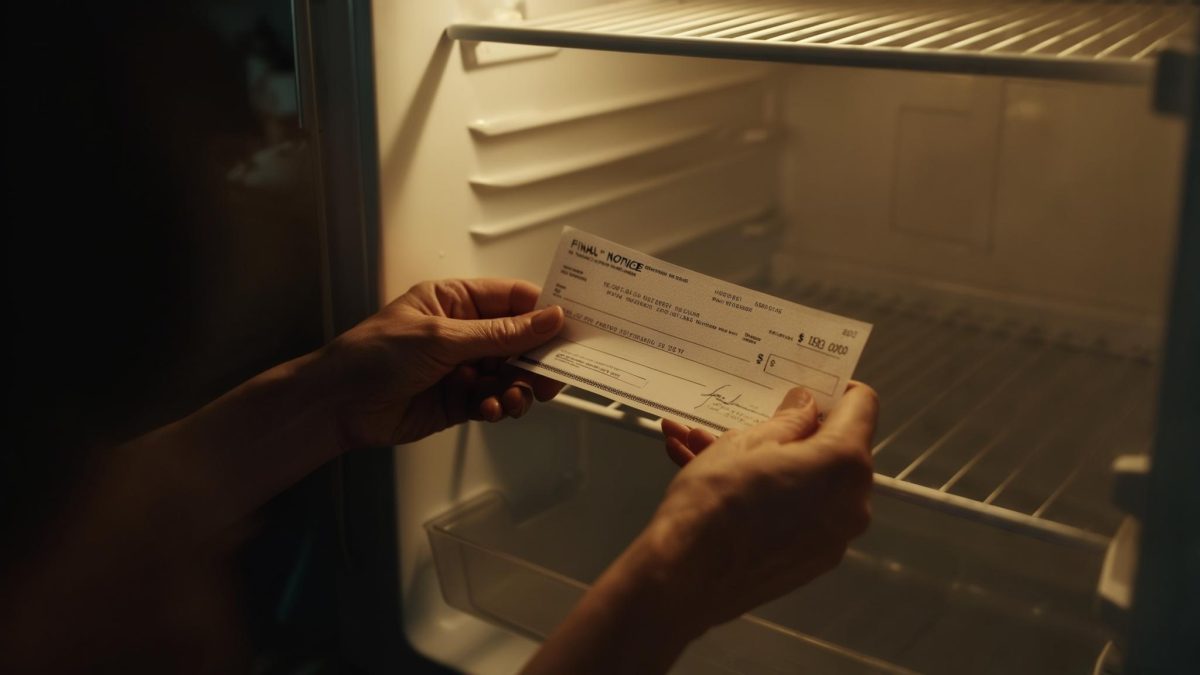

The reality arrived about three weeks later, in the form of a notice from the Georgia Division of Family and Children Services. His household’s gross monthly income — now roughly $4,250 from his salary alone, before Daria’s variable earnings — had crossed the SNAP gross income limit for a family of five, which sits at approximately $3,955 per month as of federal fiscal year 2025, per the USDA Food and Nutrition Service. Their benefits would end the following month.

The $9,000 raise, after federal and state taxes, netted Benny approximately $540 additional dollars per month. The SNAP benefits that disappeared were worth $612 per month. On paper, the raise left his family $72 in the hole every single month — before accounting for anything else that changed.

Lifestyle Inflation Moved In Before the Math Did

Here is where Benny’s own candor makes the story. He did not tell me he was blindsided by lifestyle inflation — he told me he watched it happen and could not stop it. The raise arrived and, almost immediately, small decisions shifted.

He leased a used Honda CR-V in November 2024 — $387 a month — reasoning that the family’s aging Civic had 141,000 miles and the twins were starting to cramp in the back seat. He and Daria started ordering DoorDash twice a week instead of once. Maya asked about soccer camp in the spring and he said yes without the usual hesitation. None of these decisions were reckless in isolation. Together, they added roughly $680 a month in new spending.

Childcare was the other wall. The twins attend an after-school program at $460 per child per month. Maya’s care runs $920 a month at a different facility closer to her school. That total — $1,840 a month — had been partially offset when SNAP kept grocery costs down. With SNAP gone, grocery spending jumped to roughly $900 a month for five people. The margin that the raise was supposed to create had fully evaporated by January 2025.

He pulled up the spreadsheet on his phone and showed me the January column. After rent ($1,650), childcare ($1,840), the new car payment ($387), groceries ($900), utilities ($240), and minimum payments on roughly $6,200 in credit card debt he had accumulated across 2023 and 2024, he had $214 left before any incidental expense. The emergency fund he had imagined in the parking garage remained at $340 — the same as it had been for eight months.

The Child and Dependent Care Tax Credit — a Partial Lifeline He Almost Missed

When I asked Benny whether he had looked into any tax relief tied to childcare costs, he paused. He had heard of the Child and Dependent Care Tax Credit but assumed his income was too high to benefit meaningfully. He was wrong about that — though the benefit is more modest than many families expect.

For tax year 2024, the federal Child and Dependent Care Credit allows families to claim a percentage of up to $6,000 in qualifying expenses for two or more children. At Benny’s adjusted gross income level, the applicable percentage is 20 percent, according to IRS Topic 602. That works out to a credit of up to $1,200 — not nothing, but spread across twelve months, it amounts to $100 per month in tax year relief.

His tax preparer also flagged that he may have been eligible to contribute to a Dependent Care FSA through his employer — a pre-tax benefit that allows families to set aside up to $5,000 annually for qualifying childcare costs. Benny had skipped the open enrollment window in October 2024, two weeks after the raise came through. “I didn’t even open the benefits email,” he admitted. “I thought nothing had changed.”

Where Things Stand Now, and What Benny Says Out Loud

When I last spoke with Benny in late March 2025, the car lease was two months in and he was not planning to reverse it — breaking it early would cost more than continuing. The credit card balance had climbed to $7,400. The emergency fund, after a $180 car registration fee in February, sat at $160.

He is not despairing, exactly. He described his emotional state to me as “calculating” — running scenarios, looking at whether Daria can pick up a second part-time job once the twins start first grade in August and after-school costs drop slightly. He has already submitted the Dependent Care FSA enrollment form for the next benefits year, which opens in September.

The guilt piece is something he returned to more than once across our two conversations. As the analytical member of the household, he carries the weight of the spreadsheet internally. When Maya asked for soccer camp and he said yes, it was not carelessness — it was a father who had said no enough times that yes felt like a moral obligation. That emotional dynamic, he acknowledged, is as responsible for the financial gap as any cliff in the benefit structure.

“The system doesn’t make it easy to move up,” he told me, gathering his jacket to leave the coffee shop. “But I also have to own the part where I moved up in my head before I moved up in the bank account.”

According to the USDA’s SNAP eligibility guidelines, households that fall just above the gross income threshold have no access to a graduated reduction — benefits end fully. There is ongoing policy discussion at the federal level about restructuring SNAP’s income cliff into a phased reduction, but as of this writing, no legislation has passed. For families like Benny’s, the math remains exactly as blunt as he described it in that SSA waiting room: one number crosses a line, and an entire category of support disappears overnight.

I think about Benny’s color-coded spreadsheet when I read aggregate data about the benefits cliff. The data shows households. The spreadsheet shows a father counting to $214.

Related: A $200-a-Month Raise Cost This Firefighter $3,600 a Year in Benefits — Here’s What Happened

Related: A Pittsburgh Mom Lost $600 a Month in Overtime — Then Found $3,847 in Tax Credits She Almost Missed

Leave a Reply