Roughly one in five workers’ compensation claims filed in the United States is either denied or disputed at the initial stage, according to estimates from state labor advocacy groups — and for lower-income workers without legal representation, that first denial is often the last word they hear. For Rochelle Espinoza, a 35-year-old bank teller from Charlotte, North Carolina, that statistic stopped being abstract on a Tuesday afternoon in September 2024.

A financial counselor named Patricia Okafor connected me with Rochelle in late January 2026. Patricia told me that Rochelle’s situation was one of the clearest examples she had seen of what she called “compounding system failures” — cases where one bad outcome triggers another and another, until the person at the center is holding a pile of denied claims and past-due notices. I drove to meet Rochelle at a coffee shop near her apartment in the University City neighborhood of Charlotte. She arrived five minutes early, in her bank uniform, on her lunch break. Her two-year-old daughter Naya was at daycare.

The Injury Nobody Wanted to Own

When I sat down with Rochelle Espinoza, the first thing she did was show me a photograph on her phone. It was a dark, blurry image of a wet concrete floor near the entrance to a bank vault storage corridor — taken the same afternoon she fell. She had twisted her left knee badly enough that a coworker drove her to urgent care, where doctors diagnosed a partial medial collateral ligament tear.

“I took that picture because something told me to,” Rochelle told me. “I didn’t know anything about workers’ comp. I just knew I needed to document it.”

The injury happened on September 17, 2024. Rochelle filed a workers’ compensation claim through her employer’s HR department the following week. By November 4, 2024, she had a denial letter in her mailbox. The reason cited: the insurer’s adjuster concluded the fall could not be confirmed as work-related and that her knee condition “may have predated the incident.”

Rochelle told me she had no prior knee injury, no doctor’s visits for knee pain, and no history that would support the adjuster’s reasoning. She had the photograph. She had a coworker who witnessed the fall. She had a same-day medical report. None of it was enough. According to the U.S. Department of Labor’s Office of Workers’ Compensation Programs, workers who receive an initial denial have the right to appeal — but the process is lengthy, often requires legal help, and is not guaranteed to succeed.

Rochelle could not afford an attorney. She works as a bank teller earning approximately $34,000 a year. After rent, childcare for Naya, and basic expenses, she estimated she had roughly $180 left over each month before the injury. She said she looked into contingency-fee attorneys but was told her case, without a permanent disability determination, was not likely to be profitable enough for most firms to take on.

The Bills That Kept Coming

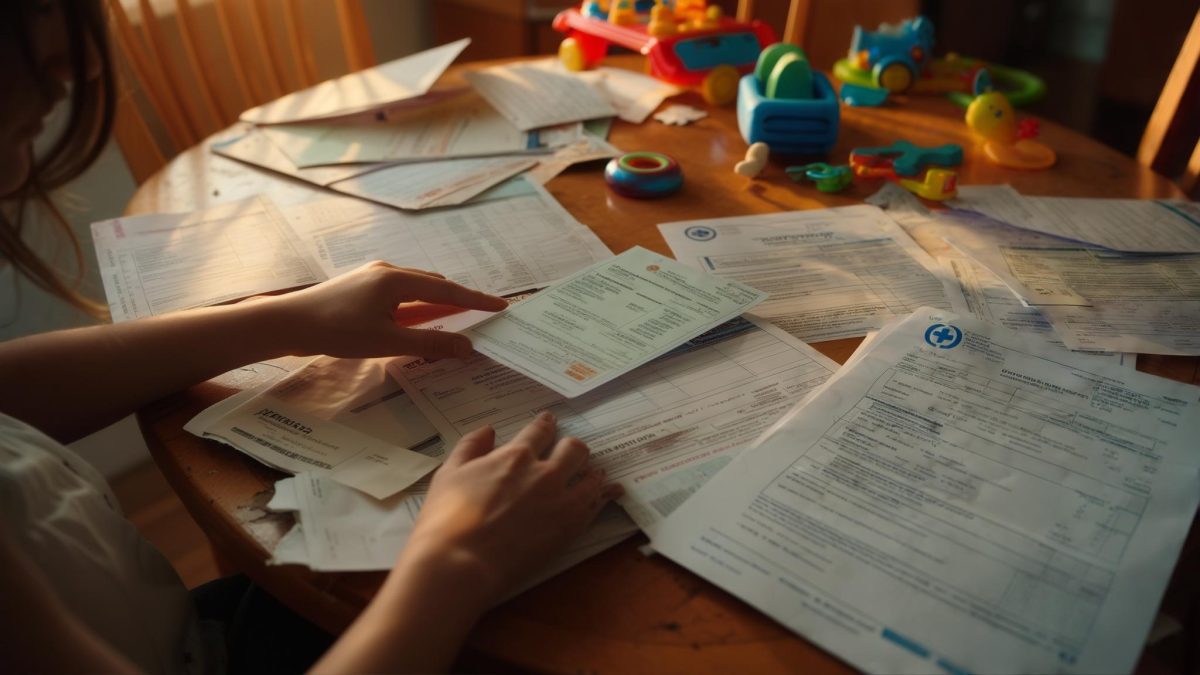

The medical costs from Rochelle’s injury accumulated faster than she had anticipated. The urgent care visit on September 17 was followed by an MRI ordered by a specialist in early October 2024. Physical therapy was recommended — two sessions per week for six weeks.

Rochelle’s employer-sponsored health insurance covered a portion of the costs, but her plan carried a $2,500 deductible. She paid $1,100 out of pocket before hitting her deductible cap, plus copays and one bill from a physical therapist who was listed as in-network but billed separately as out-of-network. By December 2024, she had $4,380 in medical debt across three providers. She stopped physical therapy after four sessions because she could not cover the $65-per-visit cost.

She told me she tried to negotiate payment plans with each provider but found the billing departments gave inconsistent information. One provider offered a zero-interest payment plan. Another sent her to collections after 90 days, which damaged her credit score. The third reduced her bill by $400 after she applied for a financial hardship waiver — a program she said she only learned about by accident, from a coworker who had gone through something similar.

Then the Insurance Letter Arrived

If the workers’ comp denial was a hard blow, what came in January 2025 was the one that made Rochelle question whether things could get worse. Her renters’ insurance carrier — she rented a two-bedroom apartment — sent a non-renewal notice dated January 14, 2025. The reason: a water damage claim she had filed in August 2024, six weeks before her injury, when a pipe fitting in her bathroom failed and soaked the floor and part of a wall.

That August claim had been paid out — the insurer covered $1,850 in damage. But as Rochelle explained to me, the claim went on her record, and when her policy came up for renewal, the carrier declined to continue coverage. She was not told this was a possibility when she filed the original claim.

Rochelle scrambled to find a new policy. She called four insurers over three days. Two declined to quote her because of the recent claim. One offered her a policy at $94 per month — compared to the $41 per month she had been paying. She took it, because she had no other option and because her lease required renters’ insurance. That $53-per-month increase represented nearly 30 percent of her monthly discretionary budget.

“That was the moment I cried,” she told me. “Not the workers’ comp letter. The insurance letter. Because I had done everything right with that pipe — I reported it immediately, I cooperated, I was honest. And they still dropped me.”

Turning to Programs She Never Expected to Need

By February 2025, Rochelle had begun quietly researching assistance programs. This was not something she did easily. As she described it to me, she had spent her whole adult life telling herself she was not “that person” — the one who needed government help. She had a job. She paid taxes. She had built her life around not asking.

But her daughter Naya was two years old. Naya’s father had not provided any financial support since leaving in late 2023. Rochelle had not pursued a formal child support order because, as she told me, she was afraid of the conflict and did not know where to start.

When Rochelle told me about applying for SNAP, she paused and looked at her coffee cup for a moment. “I didn’t tell anyone at work,” she said. “I still haven’t. I don’t know why I feel ashamed about it. I think I just always thought it was for people who made bad choices. And then I realized — I didn’t make bad choices. I fell on a wet floor.”

According to the USDA’s SNAP eligibility guidelines, a household of two with a gross monthly income below 130 percent of the federal poverty level — roughly $2,311 per month in 2025 — may qualify for benefits. Rochelle’s take-home pay after taxes and her daughter’s daycare subsidy kept her just within the eligibility threshold.

Where Things Stand Now

When I met Rochelle in January 2026, she was 16 months past the injury and still waiting on the outcome of her workers’ comp appeal, which she had filed pro se — meaning without an attorney — in March 2025. The process had involved submitting additional medical documentation and a written statement. She had not received a hearing date as of our conversation.

Rochelle told me she was not angry — or at least she had decided not to be. “Angry takes energy I need for Naya,” she said. The child support filing was in process. Patricia, her financial counselor, had helped her draft a formal dispute letter to the collections agency handling the physical therapy bill. Progress was slow, and measured in small corrections rather than victories.

As I drove back from Charlotte, I kept thinking about that photograph on Rochelle’s phone — the blurry wet floor that started everything. She had taken it instinctively, without knowing what it would mean. The image existed. The injury existed. The system just never confirmed that those two things were connected in a way it was obligated to act on.

Rochelle Espinoza is not a cautionary tale in the traditional sense. She did not overspend or ignore warnings or make a decision she now regrets. She slipped. And then she learned, one denial letter at a time, exactly how much slack there was in the safety net she had always assumed was there.

Leave a Reply