According to the Kaiser Family Foundation’s 2024 Employer Health Benefits Survey, the average annual premium for employer-sponsored family health coverage hit $25,572 — and when a worker loses access to that employer contribution, COBRA shifts nearly that entire cost onto the family. For millions of Americans, that single transition can be the event that cracks an otherwise stable household budget wide open.

I met Aisha Guzman on a Tuesday morning in late February 2026, outside a BP station off I-95 in Jacksonville, Florida. She was standing behind me in line for the pump, phone pressed to her ear, and I caught just enough of the conversation to know something was seriously wrong. She was reading numbers to someone — monthly costs, it sounded like — and her voice had the flat, rehearsed quality of someone who had said the same things so many times they had stopped feeling them.

When she hung up, I introduced myself. She shrugged and said, “Sure, why not. It’s not like talking about it makes it worse.” We ended up in the parking lot for nearly two hours.

The Life That Looked Fine From the Outside

Aisha Guzman is 29 years old, married, and the mother of three children under the age of seven. Her husband, Marcus, stays home full-time to care for the kids — a decision the couple made when their youngest was born in 2024, and Jacksonville’s childcare costs for three children would have consumed most of a second income anyway. Aisha is the sole earner, pulling in roughly $72,000 a year as a warehouse supervisor for a regional logistics company.

By most definitions, that puts the family in the upper-middle range for a household their size in Jacksonville. But income alone, Aisha told me, stopped telling the full story about eighteen months ago.

In the fall of 2024, Aisha switched employers. She left a larger distribution company that offered heavily subsidized family health coverage and took a supervisory role with a smaller logistics firm that offered better pay but a weaker benefits package. For the first several months, she was covered under her previous employer’s COBRA continuation plan while she waited for her new employer’s open enrollment window.

“I knew COBRA was going to be expensive,” she told me, leaning against her car. “I just didn’t understand that expensive meant more than my rent.”

The COBRA Cliff That Nobody Warned Her About

Under the Consolidated Omnibus Budget Reconciliation Act, employees who lose workplace health coverage can continue that coverage for up to 18 months — but they pay the full premium that the employer was previously subsidizing, plus a 2% administrative fee. For Aisha’s family of five, that meant the roughly $320 her previous employer had deducted from her paycheck each month ballooned to $2,140.

Aisha’s new employer’s open enrollment didn’t come around until January 2025. That meant roughly three months on COBRA — nearly $6,420 in premiums alone. She paid it. “We have three small kids,” she said. “I wasn’t going to gamble on nobody getting sick.”

When enrollment finally opened, the new employer’s family plan came in at $890 a month — still steep, but manageable compared to COBRA. The problem was that the deductible reset, and the plan’s network excluded the pediatrician her youngest had been seeing since birth. Switching doctors meant new referrals, new wait times, and what Aisha describes as a month of administrative chaos that she had to manage while working forty-plus-hour weeks.

The Car, the Loans, and a Budget That No Longer Adds Up

The COBRA episode didn’t happen in isolation. In December 2024, Aisha’s 2017 Honda Pilot — the family’s only vehicle — developed a transmission problem. The repair estimate from two different shops came back at $3,400. She didn’t have $3,400 liquid.

She and Marcus had been carrying roughly $61,000 in federal student loan debt from Aisha’s master’s degree in supply chain management, completed in 2022. Her monthly income-driven repayment amount had been set at $387 based on her income at the time she enrolled. That’s now $387 a month going out toward a balance she hasn’t seen meaningfully shrink.

Without the car, she was taking Ubers to her overnight supervisor shifts — about $22 each way, four nights a week. That added up to roughly $700 in rideshare costs in January alone before Marcus’s brother lent them a pickup truck they could use temporarily.

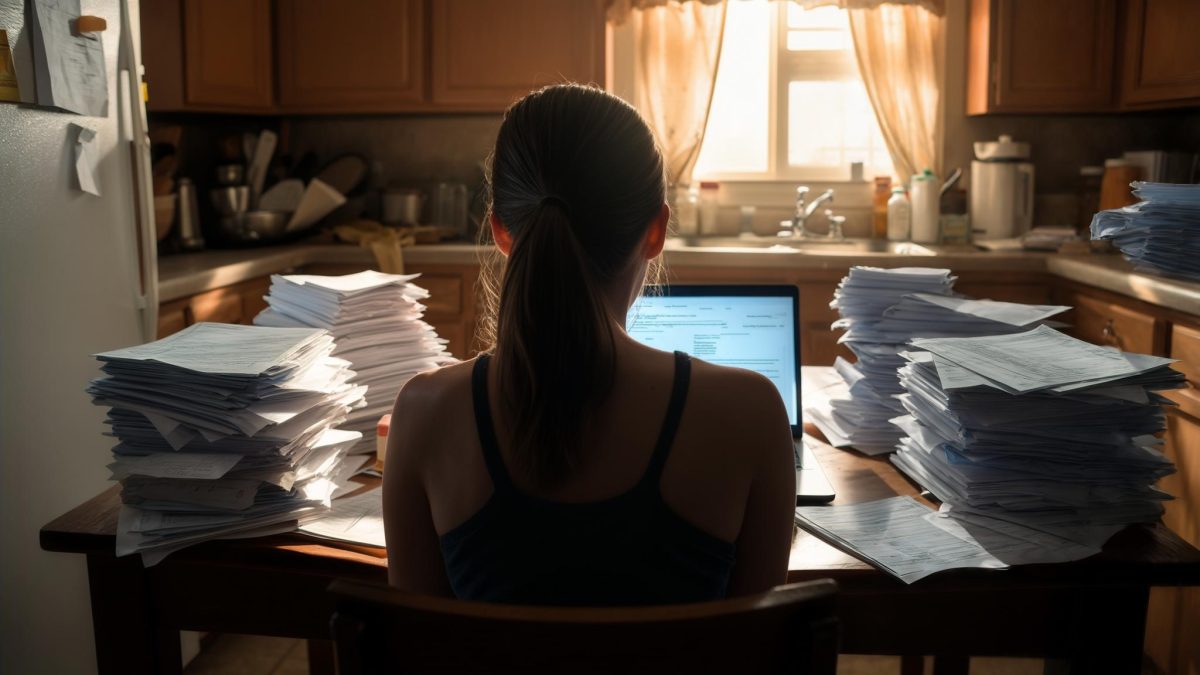

As Aisha explained to me, the math on her monthly budget has become something she avoids looking at directly. “I know roughly what’s coming in and roughly what’s going out and I know they’re too close,” she said. “I stopped putting it in a spreadsheet because seeing the actual numbers makes it harder to function.”

The Emotional Arithmetic of Getting Numb

What struck me most about Aisha during our conversation was not distress — it was the absence of it. She didn’t cry. She wasn’t angry. She recited figures the way someone reads from a utility bill, with no more emotion than the task requires. When I asked her how she was doing, emotionally, she took a long pause.

“Honestly? I feel like I’m in autopilot,” she said. “I go to work, I come home, I handle whatever the next thing is. I think at some point your brain just decides to stop reacting because the reacting doesn’t change anything.”

She holds a master’s degree. She has a career. She is, by standard measures, doing well. That, she told me, is part of what makes it disorienting. “People see my job title and assume things are fine. And on paper there’s an argument that things are fine. But fine on paper doesn’t mean you have room to breathe.”

The COBRA period had one lasting effect she hadn’t anticipated: it depleted most of the $4,800 she and Marcus had in a small emergency fund. When the car broke down two months later, there was almost nothing left to draw on. She is now rebuilding that cushion — slowly — while simultaneously servicing the student loans and covering a health premium that, even at its current reduced level, consumes more than 14% of her gross monthly income.

According to the U.S. Department of Health and Human Services, a family of five earning $72,000 may qualify for subsidized coverage through the ACA Marketplace depending on how employer coverage is structured and whether the employer plan meets affordability thresholds. Aisha was unaware of this when she enrolled in COBRA. She found out only later, through a coworker.

Where Things Stand Now, and What She Carries Forward

When I spoke with Aisha in February 2026, the Honda Pilot was still sitting in her parking lot, unrepaired. Marcus’s brother’s truck had become a longer-term arrangement than anyone planned. She had saved roughly $1,100 toward the $3,400 repair — about a third of the way there, at a pace she estimated would take until summer if nothing else came up.

Her student loan balance stood at approximately $58,700. Her income-driven repayment plan is up for recertification in August 2026, and because her income has increased since she last recertified, she expects her monthly payment to go up. She isn’t sure by how much.

When I asked Aisha what she wished she had known before making the job switch, she was quiet for a moment. “I wish someone had sat me down and explained COBRA like it was a real number,” she said. “Not a percentage. An actual dollar amount. Because if I had known it was going to cost me $2,140 a month, I would have done something differently. I don’t know what. But something.”

She paused and looked at the pump clicking off. “The thing is, I’m not even asking for sympathy. I’m just saying the system has a lot of gaps and they happen to be exactly where people like me tend to fall.”

I watched her drive away in the borrowed truck, and I kept thinking about that word — gaps. Not catastrophes, not crises by the definitions we usually assign those words. Just gaps: between what a job change requires and what a family is prepared to absorb. Between the cost of staying covered and the cost of everything else. Aisha Guzman is not in freefall. She is doing the next thing, and the thing after that, with the controlled steadiness of someone who has decided that feeling less is the only way to keep moving.

That, too, is a cost that doesn’t show up in any monthly budget.

Related: She’s 60, Self-Employed, and Just Found Out Her Social Security Estimate Was Off by $400 a Month

Related: The Workers’ Comp Denial That Cost Aisha Jeffries More Than $14,000 — and How She’s Still Rebuilding

Leave a Reply